Running a tenant credit check involves a structured process that includes obtaining consent, collecting accurate details, verifying identity, selecting a credit reporting agency, and generating a tenant credit report to evaluate financial reliability. This process costs between $25 and $75 per report, is often paid by the applicant, and includes key data such as credit score, payment history, and public records that directly support risk assessment. By combining these steps with a thorough data review, property managers can make informed decisions, reduce screening risks, and select tenants more likely to pay rent consistently.

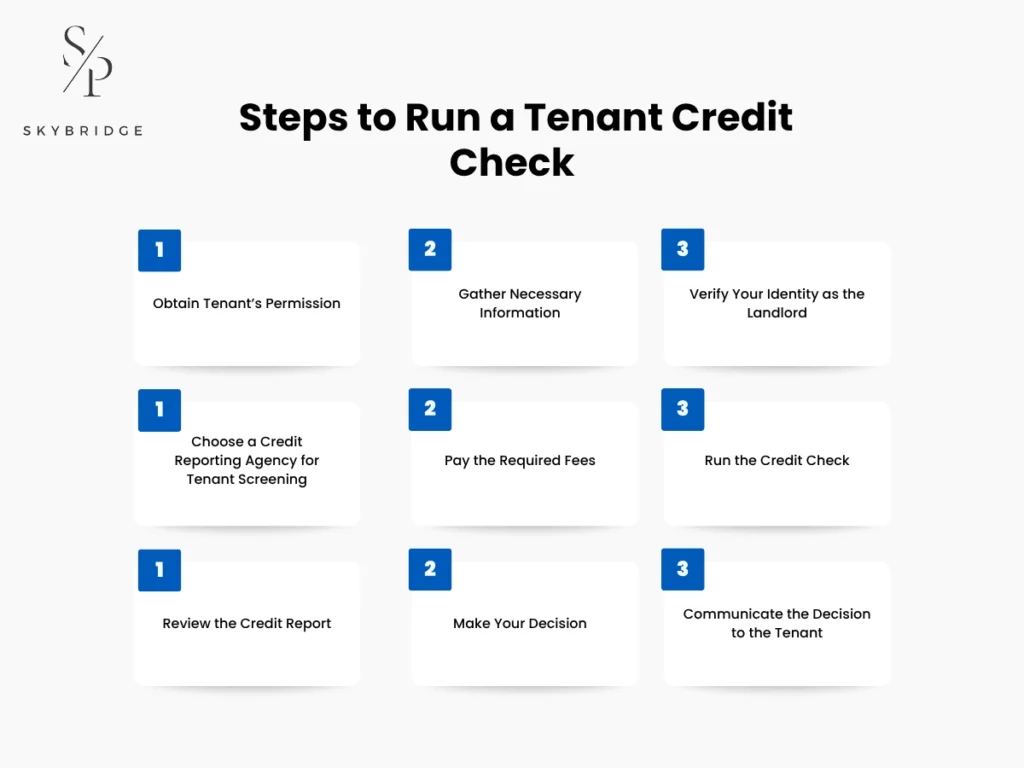

9 Steps to Run a Tenant Credit Check Effectively

- Obtain Tenant’s Permission: Secures written tenant consent to legally access a credit report and comply with FCRA requirements.

- Gather Necessary Information: Collects accurate personal, financial, and rental details to ensure a valid tenant credit report.

- Verify Your Identity as the Landlord: Confirms landlord authorization with the credit agency to securely access tenant credit data.

- Choose a Credit Reporting Agency for Tenant Screening: Select a reliable credit reporting agency to ensure accurate data and compliant screening.

- Pay the Required Fees: Covers required costs to access verified tenant credit reports without delays.

- Run the Credit Check: Submits tenant details through a screening platform to generate the credit report.

- Review the Credit Report: Examines credit score, payment history, and debt to assess financial reliability.

Obtain Tenant’s Permission

Obtaining a tenant’s written permission is legally required before running a credit check, as laws like the Fair Credit Reporting Act (FCRA) require clear consent to access a tenant’s credit report. A landlord must obtain approval before conducting a tenant credit check, as credit bureaus will not release a tenant’s credit report without verified consent. This step protects tenant privacy and keeps the tenant screening process compliant.

Clear consent procedures ensure the credit check request is accepted and reduce the risk of legal or application issues. A consent clause can be added to the rental application, or a separate form can state that a tenant’s credit and background check will be performed. The tenant must sign and date the form, identity details should be verified, and the document should be stored securely. Digital tools from tenant screening services can track approvals and support a smooth, compliant credit-check process.

Gather Necessary Information

Before running a credit check, the property manager or landlord must collect complete and accurate tenant details such as full name, Social Security number or ID, current address, employment information, and income details to ensure the credit report matches the correct individual. A credit reporting agency relies on this data to generate a valid tenant credit report, and even small errors can lead to mismatched records or delays in the tenant credit check process.

Once this information is collected, additional details should be gathered to strengthen the tenant screening process. This includes identity details (date of birth, government ID), address history, financial data such as employer name, monthly income, and existing debt (e.g., credit card balances), as well as rental history from a previous property manager. Asking the right details through essential tenant screening questions also helps complete a reliable tenant screening report and ensures a smooth tenant credit verification process.

Verify Your Identity as the Landlord

Verifying the landlord’s identity is a mandatory step that allows access to a tenant’s credit report, as credit reporting agencies must confirm that the request comes from an authorized property owner or manager and adhere to the Fair Credit Reporting Act (FCRA) before approving a tenant’s credit check. This step serves as a gateway in the tenant screening process, as credit bureaus reject requests not linked to a verified source. It also protects sensitive financial data and ensures compliance.

To complete verification, landlords must submit identity and business details to the credit reporting agency or tenant screening service, where the information is reviewed and matched with property or business records. This includes a government-issued ID, proof of property ownership or management, and contact details. Some agencies may also require business or site verification to confirm legitimacy, prevent fraud, and ensure the credit check process runs without delays.

Choose a Credit Reporting Agency for Tenant Screening

Running a tenant credit check requires choosing a reliable credit reporting agency, as the agency’s accuracy determines the tenant credit report and directly affects screening decisions. You should select an agency that complies with the Fair Credit Reporting Act (FCRA), provides complete, up-to-date credit data, and supports a consistent tenant screening process. Poor data quality can lead to wrong approvals, missed risks, or compliance issues.

Since screening decisions depend on this data, selecting the right agency requires checking accuracy, report detail, and reliability. A strong agency should provide comprehensive tenant screening reports, including credit history, rental history, and background check data, all within a single system. Many property managers use agencies linked to Experian, Equifax, and TransUnion for broader, verified data, which helps ensure accurate decisions and a compliant tenant credit-check process.

Pay the Required Fees

Processing a tenant credit check incurs required fees, as credit reporting agencies charge for accessing and generating a verified tenant credit report before it is released. Payment is part of the standard process, in which a landlord or property management company on behalf of landlord pays upfront to obtain accurate data from credit bureaus and tenant screening services. This step ensures access to reliable financial records needed to evaluate a tenant’s creditworthiness.

Since access depends on payment, understanding the fee structure helps avoid delays. Fees range from $25 to $75 per report, based on the provider and report detail. Basic reports cost less, while full tenant screening reports that include credit history, rental history, and background checks cost more. Fees may be charged per report or through a subscription plan. Paying for a trusted service ensures access to verified data and supports accurate, compliant tenant-screening decisions.

Run the Credit Check

Executing the tenant credit check is the step where landlords submit verified tenant information through a screening platform to generate a detailed tenant credit report for evaluation. This process connects to a credit reporting agency, where the tenant’s data is matched with credit bureau records to produce an accurate report. Entering correct information and selecting the right report type helps avoid errors or delays in the tenant credit check process.

Once the report is available, the focus shifts from processing to evaluation of the tenant’s financial profile. You should review key details such as credit score, payment history, outstanding debt, and any negative records, such as late payments or collections. Some reports may also include rental history and background check data. Reviewing this information carefully ensures an accurate tenant screening process and supports informed rental decisions.

Review the Credit Report

Running a tenant credit check involves carefully reviewing the credit report to identify financial patterns, assess risk levels, and determine whether the tenant meets rental criteria. A landlord should begin by analyzing the credit score, with scores above 700 generally indicating low risk, 650–700 indicating moderate risk, and below 650 indicating higher risk. This should be followed by reviewing payment history for consistency, checking outstanding debt levels, and identifying negative records such as late payments, collections, or defaults, all of which directly impact financial reliability.

After evaluating these elements, the report should be interpreted as a complete financial profile rather than in isolation. A strong score with consistent payments and manageable debt signals reliability, while frequent missed payments or high debt levels may indicate potential risk. Comparing these findings with income and rental history, as well as the tenant screening report, ensures accuracy and supports well-informed screening decisions.

Why is Running a Credit Check Essential for Landlords?

Running a tenant credit check is a crucial step in the tenant screening process because it helps landlords identify financial risk early and make informed rental decisions that protect long-term property performance. By analyzing credit score, payment history, and debt levels, landlords gain clear insight into a tenant’s financial behavior, which directly supports accurate evaluation and action.

4 key reasons why tenant credit checks are essential:

- Reduces Financial Risk: Detects late payments, defaults, or high debt that may lead to missed rent or eviction.

- Evaluates Financial Responsibility: Uses past credit behavior to predict consistent rent payment performance.

- Enables Data-Driven Decisions: Translates verified credit data into clear approval, rejection, or conditional outcomes.

- Protects Property Investment: Maintains steady cash flow, minimizes turnover, and supports long-term asset value.

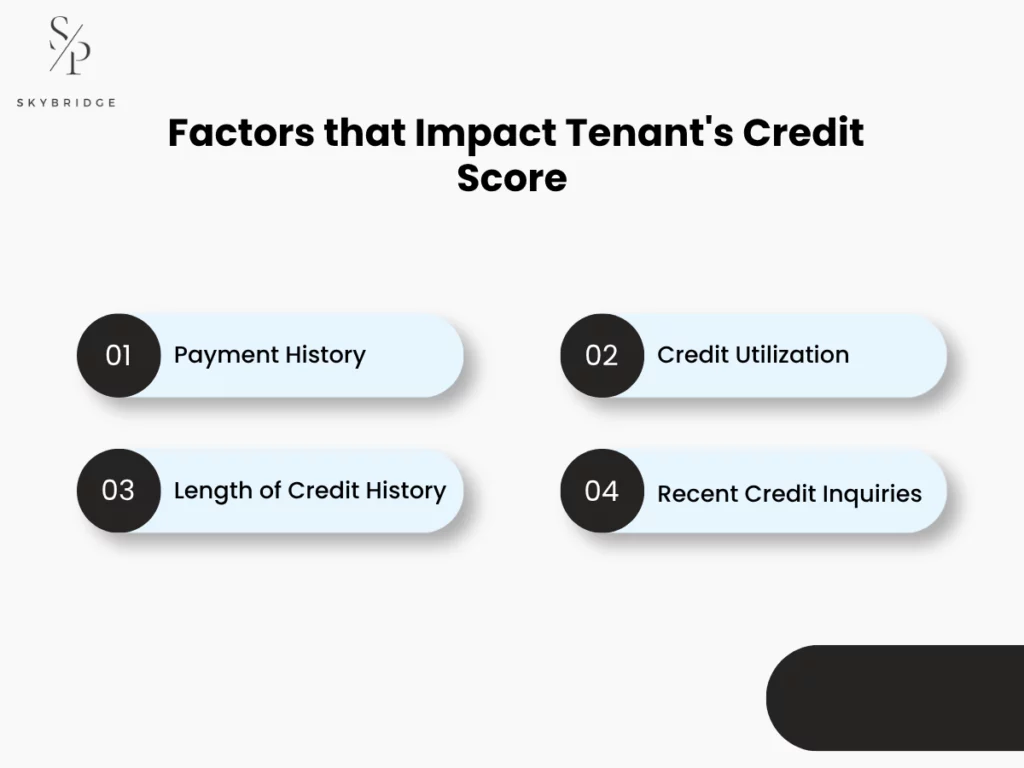

What Factors Impact a Tenant’s Credit Score?

The factors impacting a tenant’s credit score include payment history, credit utilization, length of credit history, and recent credit inquiries. Together, these factors reflect overall financial behavior, credit usage patterns, and the level of risk assessed by credit bureaus. Understanding these factors helps property managers interpret a tenant’s credit report more accurately and make better tenant-screening decisions.

4 common factors that impact a tenant’s credit score:

Payment History: Reflects how consistently a tenant pays obligations on time (35% of the score), making it the strongest indicator of future rent payment reliability.

Credit Utilization: Measures how much credit a tenant uses compared to their limit (30% of the score), where higher usage lowers the score and signals financial strain.

Length of Credit History: Evaluates how long credit accounts have been active (15% of the score), with longer histories indicating stable and reliable financial behavior.

Recent Credit Inquiries: Tracks how often a tenant applies for new credit (10% of the score), where frequent inquiries can lower the score and indicate higher financial risk.

- Payment History

A tenant’s payment history is the most important factor in their credit score, accounting for about 35%, as it measures how consistently they pay their financial obligations on time. Credit bureaus track on-time payments, late payments, and collections, with recent or repeated delays lowering the score while consistent payments increase it. Research shows that over 80% of renters want rent payments included, reinforcing its role in predicting future rent behavior.

- Credit Utilization

Credit utilization affects a tenant’s credit score by measuring how much of their available credit they use, which typically accounts for about 30% of the score. Credit bureaus calculate this ratio (e.g., $3,000 used out of a $10,000 limit), where higher usage, especially above 30%, signals greater reliance on credit. As utilization increases, the score tends to drop, indicating potential financial strain and raising landlords’ concerns about consistent rent payments.

- Length of Credit History

A tenant’s credit score is influenced by how long their credit accounts have been active, contributing about 15% of the total score. A longer average account age increases the score by providing more consistent financial data over time. As new accounts are added, the average age decreases, which can lower the score. For example, a 10-year history shows more stability than a 1-year history, helping property managers assess long-term payment reliability.

- Recent Credit Inquiries

By tracking how often a tenant applies for new credit, recent credit inquiries impact the credit score and account for about 10% of the total. Each hard inquiry, such as applying for a loan or a credit card, can slightly lower the score, especially when multiple inquiries occur in a short period. Frequent inquiries may indicate financial pressure, raising landlords’ concerns about a tenant’s ability to make consistent rent payments.

How Much Does a Tenant Credit Check Cost?

A tenant credit check costs between $25 and $75 per applicant, depending on the report type, level of detail, and screening provider. Basic credit-only reports start at $15–$25 and include a FICO score and credit history. Standard screening ranges from $30–$55 and adds criminal and eviction checks, while comprehensive bundles range from $50 to $120+ and include full credit, background, rental history, and identity verification. In most cases, HOAs pass this cost to applicants through rental application fees, which range from $30 to $75.

As the level of screening increases, costs rise due to the inclusion of more data sources and deeper verification. This makes report selection directly tied to the level of risk being evaluated, with basic reports suitable for low-risk applicants and standard or comprehensive reports providing better insight for higher-risk cases. Pricing may also vary between pay-per-report and subscription models, allowing property managers to choose an option that aligns with their screening volume and required level of detail.

What Are the Major Credit Bureaus for Tenant Screening?

The major credit bureaus for tenant screening are Experian, Equifax, and TransUnion, as these agencies collect and provide the credit data used in tenant credit reports. These bureaus maintain large credit databases that track payment history, credit accounts, and financial behavior, which tenant screening services then use to generate reports. Together, they form the primary data sources landlords rely on to evaluate creditworthiness and make informed tenant-screening decisions.

3 major credit bureaus for tenant screening are:

- Experian

Experian is a major credit bureau used in tenant screening that delivers detailed credit reports, including credit score, payment history, and account activity through integrated platforms. Many landlords access Experian insights via tenant screening services, which may also include rental and background data. Pricing ranges from $30 to $40, with basic credit-only reports on the lower end at $10 to $30, and bundled screening reports costing more, from $30 to $50, due to added data and verification layers.

- Equifax

As a widely used credit bureau, Equifax provides financial data, including credit scores, payment history, and debt levels, to assess tenant stability. This information is commonly accessed through screening services that combine financial records with rental and background checks to create a complete profile. Report costs range from $15 and $30, with basic credit reports priced lower from $15-$20 and mid-tier screening reports costing more, ranging from $20 to $30 due to additional data and verification.

- TransUnion

As another leading credit bureau, TransUnion provides tenant-focused insights, including credit score, payment history, and resident scoring models used to assess rental risk. Many screening platforms use TransUnion to generate combined reports that integrate credit, rental, and background data in one system. Costs range from $25 to $50, basic credit reports are lower-priced, ranging from $25-$35, while bundled screening reports cost around $45-$50 due to added data sources, risk scoring, and verification processes.

Partner with a Property Management Company for Smooth Tenant Credit Checks

Partnering with a property management company simplifies tenant credit checks by ensuring accurate screening, legal compliance, and faster decision-making through expert handling of the entire process. A reliable property management company streamlines consent, verification, and report evaluation, keeping the screening workflow consistent and efficient. As a result, fewer errors and delays occur while compliance with regulations like FCRA is maintained. This improved process allows HOAs to select better tenants, operate more smoothly, and maintain stable long-term rental income.